Financial Planning Blog

In Part 1, the complex set of rules surrounding Social Security survivor benefits was explored. Survivor benefits can be crucial in providing an economic safety net for families that lose a provider’s income. In this post, we will look at some tips for making the most of the survivor benefits potentially available to you. But first, it is important to clarify exactly what a person must do for their family to be eligible to receive Social Security survivor benefits.

Worker eligibility

- A worker generally becomes eligible for Social Security retirement benefits after earning 40 work credits--or 10 full years. Work credits are earned by working in “covered” employment (including self-employment) where Social Security taxes are paid.

- However, the amount of credits a worker must have accumulated for his dependents to receive survivor benefits depends on the age of the worker at death. The younger a worker is, the fewer credits are necessary for the family to be eligible for survivor benefits. For example, a worker under age 28 would only need 6 work credits, at age 34 it is 12 credits, and at 46 it is 24 credits. If the worker dies at age 62, 40 work credits are required--the same as for retirement benefits.

- Finally, there is a special rule allowing a deceased worker’s children and spouse caring for children to receive benefits even if the worker didn’t have the number of required credits. In this situation with dependent children, benefits are available as long as the worker simply had accumulated 6 credits (1.5 years of work) in the three years prior to death.

Planning tips

- While still alive, have the highest earner maximize their benefit. Although the majority of people choose to start their retirement benefits early, with married couples it is often wise to maximize the higher of the two benefits. This entails having the spouse with the highest earned benefit wait until 70, gaining delayed retirement credits. This maximized benefit will then be available across both spouses’ lifetimes. This is the most cost effective way to secure a healthy inflation adjusted lifetime income stream that will protect a couple from longevity risk. This strategy is most compelling when the higher earner is the older spouse, and has a shorter expected lifespan (often the male).

- Coordinate survivor and personal benefits wisely. If you are eligible for both a personal benefit off of your own work record and a survivor benefit off of a deceased spouse’s work record, you have an important opportunity maximize the long term value of the combined Social Security benefit stream. The general rule is to maximize the larger of the two benefits by waiting to start it at the most opportune time. Compare what your personal benefit will be if you wait until age 70 (maximized with delayed retirement credits) with the survivor benefit at your full retirement age (FRA—after which it will not grow). If your maximized personal benefit is the highest, delay taking it until age 70. In the meantime, start taking the survivor benefit as early as age 60 (usually as soon as you stop working), then switching to your own benefit at 70. If the survivor benefit at FRA will be the highest amount available to you, wait until FRA to start it. In the meantime, you can start your personal benefit at age 62. Using this strategy, you benefit from the largest possible retirement benefit for the longest possible time.

- Your survivor benefit may not be maximized at your FRA. If your deceased spouse started his or her benefit prior to their FRA (and many, many do), then are situations when it will not make sense to wait until FRA to start. (Remember the widow(er)’s limit provision mentioned in Part 1.) For example, if your spouse filed early enough, your benefit may never be larger than 82.5% of their PIA. Your survivor benefit may be maximized at this 82.5% a few years earlier than your FRA, and it may not make sense to wait any longer to start taking it. This is complex, so if your deceased spouse started taking retirement benefits early and you have yet to reach your FRA, contact the SSA and have them calculate when your survivor benefit will be maximized.

- Be mindful of the earnings test. In the years prior to hitting your FRA survivor benefits are subject to the earnings test. If you are still working, it may be counter-productive to start taking survivor benefits if you are going to lose $1 of benefits for every $2 you earn over the limit (in 2012 it is $14,640). Depending on the situation, it may, or may not, make sense to start receiving benefits if you are still working. It may be wise to delay starting and let your benefit get larger.

- Get married. Survivor benefits are available to married couples, not to those couples who have chosen not to tie-the-knot. Your decision not to encumber your relationship with the bonds of marriage may prove to be an expensive one, when you consider lost survivor and spousal benefits. Most unmarried couples (at least the ones I talk to) are oblivious to the availability and value of survivor and spousal Social Security benefits.

- Hold it…maybe you don’t want to get married until age 60. Make that remarried. Remarriage prior to age 60 will make you ineligible for survivor benefits off of a deceased spouse’s record. (If that remarriage ends, you will again be eligible for the survivor benefits.) If you are contemplating remarriage and you are getting close to age 60, it might just be worth waiting a few months…or years. It is possible that these survivor benefits may be more valuable than your personal benefit, or any spousal benefits available off of a new spouse’s record. The survivor benefits are also available earlier (age 60) than your personal or spousal benefits (age 62). Don’t underestimate the potential value of wisely coordinating a survivor benefit with your personal benefit.

- Keep track of your ex-spouse. If you were divorced after being married for at least 10 years, you may be eligible for a survivor benefit off of your ex-spouse’s work record, if he or she passes away. Your ex-spouse is dead, and money now starts appearing in your checking account! This may sound too good to be true, but hey, this is America. Again, remarriage prior to age 60 will make you ineligible (unless that marriage ends, also). Don’t count on the SSA to magically find you, though. You will need to contact them and prove your eligibility for a survivor benefit.

- Survivor benefits are listed on your Social Security statement. Although these are not mailed out annually like they used to be, you can always get an updated statement here. Your statement tells you what your spouse and children would be eligible for if you were to die this year.

As discussed in earlier articles, the Social Security System is designed to enhance the economic security of families, not just individuals. Social Security's structure of spousal and survivor benefits does provide a meaningful level of family income protection, but also adds significant complexity to an already complicated system. Unfortunately, a lack of understanding of the Social Security system may result in a failure to access available benefits at a critical time. In this post we want to take a closer look at the rules pertaining to benefits available to family survivors of a deceased worker.

Rules concerning survivor benefits

- A surviving spouse is entitled to a survivor benefit based off the deceased worker's Social Security earnings record. These are often referred to as "widow's benefits", but they also are available to widowers.

- The two must have been married for at least nine months prior to the death, unless the death is due to an accident.

- Remarriage before age 60 disqualifies a widow for survivor benefits. However, if that marriage ends (e.g. a divorce, death of the second spouse) the surviving spouse is again eligible for benefits off the deceased spouse's record.

- Remarriage after 60 does not cause a person to lose eligibility for survivor benefits. That person could continue to receive the survivor benefit, but may also choose to switch to their personal benefit and/or spousal benefits based off of their new spouse's earnings record.

- There is no double-dipping--a person cannot take a survivor benefit and their personal and/or spousal benefit. For example, John dies at age 70 with a $2,500/month benefit, while his 70 year old wife Mary was receiving own benefit of $1,000/month. She would drop her personal benefit and start receiving her survivor benefit of $2,500. She would not get to receive both benefits totaling $3,500.

- If a person is unlucky enough to be widowed multiple times, they are eligible for the highest of the available survivor benefits.

- There are potentially survival benefits available for divorced spouses.

- The size of the survivor benefit is determined by 1) the amount of the deceased worker's retirement benefit, and 2) the age at which the surviving spouse starts the benefits. However, there are some important adjustments and limitations that can make calculating the survivor's benefit pretty complex.

- The survivor benefit is calculated off the prmary insurance amount (PIA), which is the monthly benefit the deceased worker would have received at full retirement age (FRA). If the deceased worker's benefit had been increased with delayed retirement credits (DRCs), then this higher amount (or "deemed life PIA") is used. (This includes the situation where a worker dies past FRA without having started to receive benefits--the deemed life PIA is adjusted upward for DRCs that had been earned up to point-of-death.) What this means is that if a worker delays starting their retirement benefits and earns DRCs, the surviving spouse will ultimately be eligible for a higher survivor benefit.

- When a worker dies after receiving reduced benefits (i.e. retirement benefits were reduced for starting prior to FRA), the deceased worker's PIA is still the base for calculating the survivor benefit. However, the deceased worker's actual reduced benefit will be a limiting factor on the ultimate benefit available to the surviving spouse. This is because of an obscure, but very important rule called the widow(er)'s limit provision. The survivor benefit will never be higher than the larger of the deceased worker's actual benefit or 82.5% of the deceased's PIA. (This is meant to prevent, or at least limit, situations where the survivor benefit is higher than the actual benefit the deceased worker was receiving.) What this means is a worker's decision to take early benefits will reduce the potential survivor benefits available to their spouse.

- If the surviving spouse waits until their own FRA*, they will receive the full survivor benefit--i.e. 100% of the deceased spouse's PIA (adjusted upward for any DRCs). However, in the situation where the worker had taken early reduced benefits, the widow(er)'s limit provision basically reduces the full survivor benefit to the level of the deceased worker's actual benefit, but not below 82.5% of the PIA. (Got that?) Important to note is that unlike a person's personal benefit, there is no advantage to waiting longer--the survivor benefit will not continue to grow past one's FRA (i.e. there are no delayed retirement credits with survivor benefits).

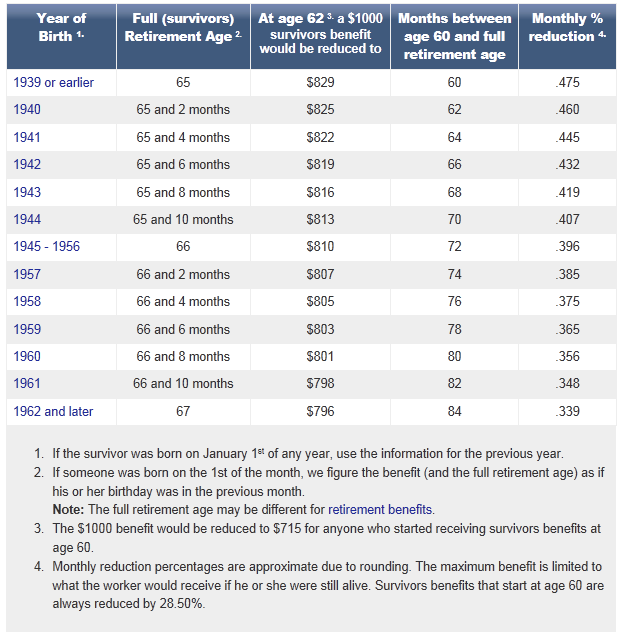

- A surviving spouse can generally start receiving benefits as early as age 60. If a surviving spouse chooses to start receiving survivor benefits prior to FRA, the benefit is reduced up to 28.5% (to 71.5% of the full survivor benefit), depending upon how early they choose to start. (See this chart for details on the exact monthly reductions by birth year.) Even if the deceased worker had started reduced benefits at the earliest age (62), and the surviving spouse starts survivor benefits at the earliest possible age (60), the survivor benefit is never lower than 71.5% of the worker's PIA.

- The survivor benefit is calculated off the prmary insurance amount (PIA), which is the monthly benefit the deceased worker would have received at full retirement age (FRA). If the deceased worker's benefit had been increased with delayed retirement credits (DRCs), then this higher amount (or "deemed life PIA") is used. (This includes the situation where a worker dies past FRA without having started to receive benefits--the deemed life PIA is adjusted upward for DRCs that had been earned up to point-of-death.) What this means is that if a worker delays starting their retirement benefits and earns DRCs, the surviving spouse will ultimately be eligible for a higher survivor benefit.

- There are some special rules that allow surviving spouses to receive benefits prior to age 60.

- If the surviving spouse is disabled, they can start receiving benefits as early as age 50. Any benefit prior to age 60 would generally be 71.5% of the PIA.

- If the surviving spouse who is not yet age 60 is still caring for the children of the deceased spouse, he or she is eligible for 75% of the deceased's PIA until the child reaches the age of 16. (Or any age if the child becomes disabled prior to age 22.)

- Surviving spouses are not the only ones entitled to benefits off a deceased person's Social Security earnings record. The deceased's children and dependent parents may also receive benefits.

- Children of the deceased worker who are under age 18 (age 19 if still in high school) are eligible for a benefit equal to 75% of the deceased worker's PIA . (The child must also be unmarried.)

- A disabled child may receive the same 75% benefit at any age, as long as he or she became disabled prior to age 22 and remains disabled.

- Believe it or not, some parents may receive benefits off of their children's earnings records. If the deceased worker was providing greater than 50% of the support for a parent over age 62, then that parent may receive a benefit of 82.5% of the worker's PIA. If both parents were supported by the deceased worker, each is entitled to a benefit of 75% of the worker's PIA. Of course, if the parents were entitled to larger benefits off of their personal records, they would continue to receive them instead. They would not be able to receive a survivor benefit and their personal or spousal benefits at the same time.

- A special one- time lump sum death payment of $255 is also available to surviving spouses who were living in the same household with the deceased worker at the time of death. If there is no spouse eligible for this benefit, it may be paid to a child (or children) eligible to receive benefits off the deceased's record.

Some limiting factors

As you can see, a number of people might be eligible to receive survivor benefits off of a deceased person's Social Security earnings record. These survivor benefits, when added together, could far exceed the benefits the deceased person would have received if they remained alive. However, there are a couple of important rules that limit the amount of benefits available to survivors.

- There is a maximum family benefit--the maximum monthly amount that can be paid on a particular worker's earnings record. This applies not only to survivor benefits, but also when a beneficiary is alive and receiving benefits. (There is a different maximum family benefit payable to a family of a disabled worker.) This is an excessively complicated formula, but the gist of it is that the family maximums range from 150% to about 180% of the deceased workers PIA.

- For example, consider a deceased worker with a PIA of $2,000/month, who leaves a surviving spouse below the age of 60, and three children under the age of 16.

- Each would be eligible for a benefit equal to 75% of $2,000, or $1,500/month. Combined these four benefits would equal $6,000/month, or 300% of the deceased's PIA.

- However, the family maximum benefit in this situation would be about 175% of the deceased worker's PIA, or $3,500/month. In such situations, each benefit is adjusted proportionately to bring the total within the limits.

- There is the earnings test--which can mean lower benefits if a beneficiary works and earns too much in a year. Just as regular retirement benefits are subject to the earnings test, so are survivor benefits. This means that if the recipient is below their FRA and they earn over the earnings limit, they would lose some (or all) of their survivor benefits. In 2012 the earnings limit is $14,640 for benefit recipients who are below FRA for the entire year. For every $2 earned above $14,640, there will be $1 of Social Security benefits deducted.

- For example, consider a person receiving $1,000/month ($12,000/year) in survivor benefits. As long as the person earns below $14,640 then there is no impact on their full $1,000/month survivor benefits. If they earn $24,640 for the year, then $5,000 of benefits will be deducted. (This is half of the $10,000 above the limit). If the person earns $24,000 or more above the limit (i.e. $38,640 or more) then their survivor benefit would be entirely lost.

- If the recipient of benefits is past their FRA, then there are no earnings limits. They can earn as much as they want and still receive 100% of the benefits to which they are entitled.

- There are special rules for the year in which a beneficiary hits their FRA.

- Only earnings from work (i.e. wages or self-employment income) count toward the earnings test. Investment earnings, pensions, and other government benefits are not counted toward the limit.

- The earnings test is on an individual, not a household level. As a result, if a surviving spouse earns above the limit it does not impact the benefits of any children also receiving benefits. Also, a person earning above the limit does not impact the Social Security benefits of their spouse.

------------------------------------------------------------------------------

*As if this isn't complicated enough, your full retirement age as a survivor may be different than your FRA for regular retirement benefits. For example, a person born in 1956 will have a survivor FRA of age 66, but a regular FRA of 66 and 4 months. This is because the birth years for the gradual FRA shifts from age 65 to 66 started in 1943 for regular benefits and in 1945 for survivor benefits. Also, the gradual FRA shift from age 66 to age 67 starts two years later-birth years 1954 for retirement benefits and 1956 for survivor benefits. (Was anyone paying attention when these rules are made?)

When mountain biking with my wife and friends, we often remind each other of a very important concept--the penalty of failure*. There is nothing quite like a big drop off the side of the trail to change the risk-reward equation when encountering a particularly technical, rocky section. Without the potential of a long, painful fall that could seriously impact our ability to enjoy future outings, we might otherwise ride the section with confidence...or at least give it a sporting attempt. It is that relatively small possibility of tumbling down a steep hillside into a rocky creek that overwhelms the depleted testosterone levels of the 50-somethings I choose to ride with. Humility is our friend.

I used to joke that helmets messed up my hair. That was before the brain surgeons shaved my head and then closed up the suture with stainless steel staples. -- Comment on blog discussing the bicycle helmet debate

Considering both the penalty of failure and the probability of failure is important in personal financial planning. If they are severe enough, the consequences of our potential failures are often more important than the probability of our success or failure. This is why we buy fire insurance for our homes, and life insurance while we are young, healthy and raising children. Although we know we will likely never cash in on the policies, the downside is just too much to risk.

Retirement planning is a key area where we should be concerned not only with the probability, but the penalty of failure. We don't just want to know what will happen if things go well, but how will we fare if things go bad. Your financial projections may look great, assuming you get reasonable returns on a consistent basis, and you don't live much beyond your life expectancy. However, what happens if market returns are significantly lower for an extended period of time, or you simply have the back luck of encountering a bear market right when you start to take large withdrawals from your retirement accounts? What happens if you (or your spouse, or both) happen to live long beyond your average life expectancy--say to age 95 or 100? In addition, what are the consequences if one of you (or both) needs expensive long term care services?

We can't eliminate all of the risk in our lives or financial plans. However, we can often mitigate the consequences of failure or bad luck. We can lessen the potential penalty of failure by implementing different strategies to secure a healthy, guaranteed minimum floor of retirement income that will last for a lifetime. For example:

- Maximize your Social Security benefits, which will give you (and your spouse) inflation adjusted benefits for across both your lifetimes.

- Consider forgoing the lump sum benefit, and take your employer pension (if you are fortunate enough to have one) as a monthly annuity with survivor benefits.

- Use some of your retirement savings to purchase low cost immediate annuities to create your own lifetime income stream--a do-it-yourself pension. Although it adds to the cost, consider buying these with inflation protection.

Even if you think the probability of needing expensive long term care is low, consider the penalty of failure. Will you have sufficient income and assets to pay for care, even if the markets don't cooperate? If the penalty of failure is simply a smaller inheritance for your children, this is an acceptable risk for most of us. However, if the penalty of failure is leaving your spouse financially insecure or destitute, than the risk is simply unacceptable. If the penalty of failure is relying on government assistance (Medicaid) you should strive to avoid it by proper planning. Although we may not eliminate this risk, we can mitigate the consequences by purchasing a reasonable level of long term care insurance, or by dedicating sufficient assets to pay for any necessary care.

If you study enough financial planning literature, you are bound to come across references to Pascal's Wager. Blaise Pascal was 17th century French philosopher, who reasoned that although it was impossible to prove the existence of God, it was a smart wager to believe in Him when a person considers the consequences of the decision. When you weigh the costs, benefits, risks and rewards, it is certainly a much better bet to put faith in God than to join with the non-believers. Although I suspect that financial writers have taken considerable license in adapting Pascal's reasoning to modern day risk management, that isn't critical for our purposes. The key point is that in making decisions, avoiding unacceptable outcomes (e.g. eternity in hell or moving in with your in-laws) should be a top priority.

When making our personal plans, we would all be wise to consider the sage advice of respected author, investment advisor, and former Oregon neurologist William Bernstein: "Always consider Pascal's Wager: What happens to my portfolio--and my future--if my assumptions are wrong?" You can count on him for a consistent reminder that, "The name of the game with retirement planning is not to get rich. Instead, the goal is to not be poor."

You can also bet he has a strong opinion on wearing bike helmets.

----------------------------------------------

*Miles lived to ride another day. See him after the crash.

Next page: Disclosures

{kind=link}