Financial Planning Blog

Social Security Survivor Benefits – The Rules (Part 1)

Social Security Survivor Benefits – The Rules (Part 1)

As discussed in earlier articles, the Social Security System is designed to enhance the economic security of families, not just individuals. Social Security's structure of spousal and survivor benefits does provide a meaningful level of family income protection, but also adds significant complexity to an already complicated system. Unfortunately, a lack of understanding of the Social Security system may result in a failure to access available benefits at a critical time. In this post we want to take a closer look at the rules pertaining to benefits available to family survivors of a deceased worker.

Rules concerning survivor benefits

- A surviving spouse is entitled to a survivor benefit based off the deceased worker's Social Security earnings record. These are often referred to as "widow's benefits", but they also are available to widowers.

- The two must have been married for at least nine months prior to the death, unless the death is due to an accident.

- Remarriage before age 60 disqualifies a widow for survivor benefits. However, if that marriage ends (e.g. a divorce, death of the second spouse) the surviving spouse is again eligible for benefits off the deceased spouse's record.

- Remarriage after 60 does not cause a person to lose eligibility for survivor benefits. That person could continue to receive the survivor benefit, but may also choose to switch to their personal benefit and/or spousal benefits based off of their new spouse's earnings record.

- There is no double-dipping--a person cannot take a survivor benefit and their personal and/or spousal benefit. For example, John dies at age 70 with a $2,500/month benefit, while his 70 year old wife Mary was receiving own benefit of $1,000/month. She would drop her personal benefit and start receiving her survivor benefit of $2,500. She would not get to receive both benefits totaling $3,500.

- If a person is unlucky enough to be widowed multiple times, they are eligible for the highest of the available survivor benefits.

- There are potentially survival benefits available for divorced spouses.

- The size of the survivor benefit is determined by 1) the amount of the deceased worker's retirement benefit, and 2) the age at which the surviving spouse starts the benefits. However, there are some important adjustments and limitations that can make calculating the survivor's benefit pretty complex.

- The survivor benefit is calculated off the prmary insurance amount (PIA), which is the monthly benefit the deceased worker would have received at full retirement age (FRA). If the deceased worker's benefit had been increased with delayed retirement credits (DRCs), then this higher amount (or "deemed life PIA") is used. (This includes the situation where a worker dies past FRA without having started to receive benefits--the deemed life PIA is adjusted upward for DRCs that had been earned up to point-of-death.) What this means is that if a worker delays starting their retirement benefits and earns DRCs, the surviving spouse will ultimately be eligible for a higher survivor benefit.

- When a worker dies after receiving reduced benefits (i.e. retirement benefits were reduced for starting prior to FRA), the deceased worker's PIA is still the base for calculating the survivor benefit. However, the deceased worker's actual reduced benefit will be a limiting factor on the ultimate benefit available to the surviving spouse. This is because of an obscure, but very important rule called the widow(er)'s limit provision. The survivor benefit will never be higher than the larger of the deceased worker's actual benefit or 82.5% of the deceased's PIA. (This is meant to prevent, or at least limit, situations where the survivor benefit is higher than the actual benefit the deceased worker was receiving.) What this means is a worker's decision to take early benefits will reduce the potential survivor benefits available to their spouse.

- If the surviving spouse waits until their own FRA*, they will receive the full survivor benefit--i.e. 100% of the deceased spouse's PIA (adjusted upward for any DRCs). However, in the situation where the worker had taken early reduced benefits, the widow(er)'s limit provision basically reduces the full survivor benefit to the level of the deceased worker's actual benefit, but not below 82.5% of the PIA. (Got that?) Important to note is that unlike a person's personal benefit, there is no advantage to waiting longer--the survivor benefit will not continue to grow past one's FRA (i.e. there are no delayed retirement credits with survivor benefits).

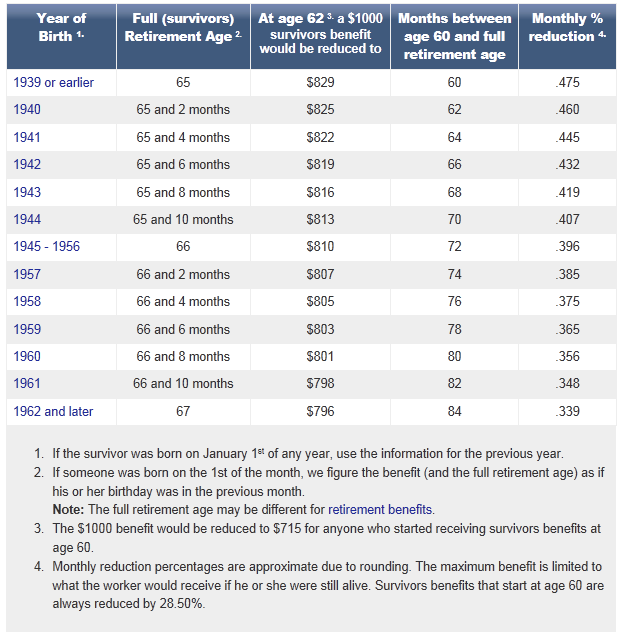

- A surviving spouse can generally start receiving benefits as early as age 60. If a surviving spouse chooses to start receiving survivor benefits prior to FRA, the benefit is reduced up to 28.5% (to 71.5% of the full survivor benefit), depending upon how early they choose to start. (See this chart for details on the exact monthly reductions by birth year.) Even if the deceased worker had started reduced benefits at the earliest age (62), and the surviving spouse starts survivor benefits at the earliest possible age (60), the survivor benefit is never lower than 71.5% of the worker's PIA.

- The survivor benefit is calculated off the prmary insurance amount (PIA), which is the monthly benefit the deceased worker would have received at full retirement age (FRA). If the deceased worker's benefit had been increased with delayed retirement credits (DRCs), then this higher amount (or "deemed life PIA") is used. (This includes the situation where a worker dies past FRA without having started to receive benefits--the deemed life PIA is adjusted upward for DRCs that had been earned up to point-of-death.) What this means is that if a worker delays starting their retirement benefits and earns DRCs, the surviving spouse will ultimately be eligible for a higher survivor benefit.

- There are some special rules that allow surviving spouses to receive benefits prior to age 60.

- If the surviving spouse is disabled, they can start receiving benefits as early as age 50. Any benefit prior to age 60 would generally be 71.5% of the PIA.

- If the surviving spouse who is not yet age 60 is still caring for the children of the deceased spouse, he or she is eligible for 75% of the deceased's PIA until the child reaches the age of 16. (Or any age if the child becomes disabled prior to age 22.)

- Surviving spouses are not the only ones entitled to benefits off a deceased person's Social Security earnings record. The deceased's children and dependent parents may also receive benefits.

- Children of the deceased worker who are under age 18 (age 19 if still in high school) are eligible for a benefit equal to 75% of the deceased worker's PIA . (The child must also be unmarried.)

- A disabled child may receive the same 75% benefit at any age, as long as he or she became disabled prior to age 22 and remains disabled.

- Believe it or not, some parents may receive benefits off of their children's earnings records. If the deceased worker was providing greater than 50% of the support for a parent over age 62, then that parent may receive a benefit of 82.5% of the worker's PIA. If both parents were supported by the deceased worker, each is entitled to a benefit of 75% of the worker's PIA. Of course, if the parents were entitled to larger benefits off of their personal records, they would continue to receive them instead. They would not be able to receive a survivor benefit and their personal or spousal benefits at the same time.

- A special one- time lump sum death payment of $255 is also available to surviving spouses who were living in the same household with the deceased worker at the time of death. If there is no spouse eligible for this benefit, it may be paid to a child (or children) eligible to receive benefits off the deceased's record.

Some limiting factors

As you can see, a number of people might be eligible to receive survivor benefits off of a deceased person's Social Security earnings record. These survivor benefits, when added together, could far exceed the benefits the deceased person would have received if they remained alive. However, there are a couple of important rules that limit the amount of benefits available to survivors.

- There is a maximum family benefit--the maximum monthly amount that can be paid on a particular worker's earnings record. This applies not only to survivor benefits, but also when a beneficiary is alive and receiving benefits. (There is a different maximum family benefit payable to a family of a disabled worker.) This is an excessively complicated formula, but the gist of it is that the family maximums range from 150% to about 180% of the deceased workers PIA.

- For example, consider a deceased worker with a PIA of $2,000/month, who leaves a surviving spouse below the age of 60, and three children under the age of 16.

- Each would be eligible for a benefit equal to 75% of $2,000, or $1,500/month. Combined these four benefits would equal $6,000/month, or 300% of the deceased's PIA.

- However, the family maximum benefit in this situation would be about 175% of the deceased worker's PIA, or $3,500/month. In such situations, each benefit is adjusted proportionately to bring the total within the limits.

- There is the earnings test--which can mean lower benefits if a beneficiary works and earns too much in a year. Just as regular retirement benefits are subject to the earnings test, so are survivor benefits. This means that if the recipient is below their FRA and they earn over the earnings limit, they would lose some (or all) of their survivor benefits. In 2012 the earnings limit is $14,640 for benefit recipients who are below FRA for the entire year. For every $2 earned above $14,640, there will be $1 of Social Security benefits deducted.

- For example, consider a person receiving $1,000/month ($12,000/year) in survivor benefits. As long as the person earns below $14,640 then there is no impact on their full $1,000/month survivor benefits. If they earn $24,640 for the year, then $5,000 of benefits will be deducted. (This is half of the $10,000 above the limit). If the person earns $24,000 or more above the limit (i.e. $38,640 or more) then their survivor benefit would be entirely lost.

- If the recipient of benefits is past their FRA, then there are no earnings limits. They can earn as much as they want and still receive 100% of the benefits to which they are entitled.

- There are special rules for the year in which a beneficiary hits their FRA.

- Only earnings from work (i.e. wages or self-employment income) count toward the earnings test. Investment earnings, pensions, and other government benefits are not counted toward the limit.

- The earnings test is on an individual, not a household level. As a result, if a surviving spouse earns above the limit it does not impact the benefits of any children also receiving benefits. Also, a person earning above the limit does not impact the Social Security benefits of their spouse.

------------------------------------------------------------------------------

*As if this isn't complicated enough, your full retirement age as a survivor may be different than your FRA for regular retirement benefits. For example, a person born in 1956 will have a survivor FRA of age 66, but a regular FRA of 66 and 4 months. This is because the birth years for the gradual FRA shifts from age 65 to 66 started in 1943 for regular benefits and in 1945 for survivor benefits. Also, the gradual FRA shift from age 66 to age 67 starts two years later-birth years 1954 for retirement benefits and 1956 for survivor benefits. (Was anyone paying attention when these rules are made?)

Next page: Disclosures

{kind=link}