Financial Planning Blog

Why Employees Hold Company Stock (Part 3)

Why Employees Hold Company Stock (Part 3)

If holding too much employer stock is so risky, and so many authorities warn against it, why do so many people continue to invest their retirement savings in the company they work for? These are the employees of America's great corporations, the engine of the world's mightiest economy--they can't all be simpletons!

If you have occasion to read books or articles on the subject of behavioral finance you will probably notice how often the issue of company stock is used as an example for a variety of behavioral biases-or ways which investors act less than rationally or optimally. Here are a few examples of relevant investor biases:

- Home bias is the tendency to believe that familiar investments are the best. Many people are simply more comfortable investing in what they perceive they know best. And, what do we know better than our own company? In Your Money and Your Brain, Jason Zweig sites a 2001 study of 401K investors where only 16.4% of them believed their company stock was riskier than the stock market as a whole. This is certainly contrary to portfolio theory and conventional wisdom that a diversified portfolio of stocks is less risky than a single stock.

- Closely related to home bias is something called ambiguity aversion bias--basically that people dislike uncertainty more than they dislike risk. A person feels they have an understanding of the risk they are taking with their own company, but haven't a clue what is going on at all those other companies, or the market as a whole. Zweig relates a funny story about how while giving a talk and cautioning investors on the perils of investing in their own company stock, and citing the recent Enron example, a guy in the audience stood up and challenged him:

I can't believe what you just said! I completely agree that any company could be the next Enron. But that's why your advice makes no sense. Why should I move my money from the one company I know everything about to hundreds of stocks I don't know anything about? Diversifying doesn't protect me from the next Enron, it exposes me to every next Enron--and the stock market is full of them! I want my money where I know it's safe--in the company I work for and the company I understand better than any other one around. That's how I control risk.

- Also mentioned is optimism bias--basically, that people are just too optimistic and refuse to believe their own company could hit the skids like Enron. The Enron type scenario will certainly happen to other poor souls, but won't happen to me.

- Somewhat related to optimism bias, is confirmation bias, where people put too much weight on information or data that supports what they want to believe. They believe positive commentary about their company and its prospects--basically because they want to believe--and discount negative news. (They drink the company Kool-Aid.) People rationalize their concentrated holdings of company stock because of "big things coming down the road". A sad example are the employees who doubled down on Enron stock in late 1999 after their human resources director responded to the question, "Should we invest all of our 401K in Enron stock?" with a resounding: "Absolutely".

- Since many investors receive company stock as a matching or profit sharing contribution, they are susceptible to the endowment effect. The endowment effect is where you value a thing or asset that you own, more than when you don't own it. Basically, even though you would likely not have purchased the company stock if you had been given the equivalent cash in the first place, you are now reluctant to sell the stock at a fair market price. Not only is there an implicit company endorsement of the stock when your company gives it to you, but there is this aversion to selling and diversifying away from it. The endowment effect is powerful--according to Vanguard, 401K plans that make matching contributions in company stock have 3.3 times more assets held in company stock than those that don't (37% versus 11%).

There are, of course, other reasons why people end up having relatively high concentrations of their employer stock. Many people participate in employer stock purchase plans where they receive a significant discount on the purchase price. There may be restrictions on how soon an employee can sell the stock, and then there are tax considerations on the sale. Other employees may receive large blocks of stock options or restricted stock, which have a vesting period and are then subject to substantial taxation. By delaying the exercise of options, or the sale of stock, the employee is delaying taxation, which is generally considered a good thing. All this employer stock can add up to a substantial percentage of a person's net worth.

Inside or outside a 401K plan, there is at least one more good reason why many hold sizable percentages of their net worth in company stock. It often works out very well for many people. Most of us know, or know of, folks who have done very well due to working for a successful company and dutifully buying and holding the company stock. Water cooler talk about how Larry bought his lake house with the money he made on stock accumulated through a share purchase plan, or how Ruth retired early after cashing in on her options, make your company stock look like a pretty smart investment. And, it just may be.

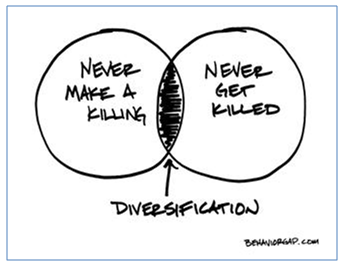

The problem with holding too much company stock isn't that you can't be successful. You obviously can be. You can be very, very successful. The problem is you can also lose big, possibly losing your job at the same time. When you hold a concentrated position in company stock (or any one stock) the range of outcomes is simply much broader (from very bad to very good) than when you are highly diversified portfolio of hundreds of stocks. Or, as Carl Richards recently described being diversified: "Never make a killing. Never get killed." When approaching the decision on how much company stock to hold, you need to decide whether you want the chance to get somewhat richer while accepting the risk of ending up significantly poorer. As for me, I would choose to diversify, hoping to have "enough" to meet my reasonable financial objectives, while minimizing the chance of ending up poor.

Next page: Disclosures

{kind=link}