Financial Planning Blog

In planning for your financial future, accounting correctly for inflation is absolutely critical. Unfortunately, thinking clearly about the impact of inflation isn't something most people do naturally. Most of us have a tendency toward what behavioral economists call "money illusion", where we think about dollars in "nominal" terms, as opposed to their "real" or inflation-adjusted value. We routinely confuse the face (nominal) value of money for its purchasing (real) value.

Here is a quick example of money illusion. Nick gets a 3% raise during a year when inflation is at 3.8% (as in 2008). Nora gets only a 1% raise during a year when inflation was actually a bit negative, such as in 2009. Who got the better deal? Most people would say Nick, whose nominal raise was three times that of Nora's. However, the real purchasing power of Nora's salary increased over 1%, while Nick's actually declined almost 1%. Despite getting a smaller nominal raise, Nora actually got a much better deal than Nick--it probably didn't feel that way.

People are just not very good at factoring in inflation as they think about their money over time. Gary Belsky and Thomas Gilovich give a couple of reasons for this in Why Smart People Make Big Money Mistakes: "First, accounting for inflation involves the application of arithmetic, which is often annoying and downright impossible for many people. Second, inflation today, at least in the United States, is an incremental affair--2 percent to 4 percent, on average, over the last decade and a half...little numbers are easy to discount or ignore."

Although it might be somewhat difficult, and the impact may seem small, accurate thinking about inflation is crucial in avoiding some big financial planning mistakes. Here are three areas where people commonly fail to consider the impact of inflation on their future:

- Projecting investments and salary forward at a nominal growth rate, but failing to adequately consider that expenses will also be going up with inflation. For example, a 50 year old couple anticipates having $2.5M saved by age 65, considering their current savings rate, anticipated raises, and portfolio growth of 7% per year. Assuming a safe 4% withdrawal rate, that means $100K of income in retirement, to be combined with Social Security of about $36K per year. Wow, that's considerably more money than they make today! Maybe they can cut back on the savings a bit, and enjoy life a bit more. What they don't understand that these anticipated investment returns factor in an expected inflation rate of about 3%. What costs $100 today will on average cost over $150 in fifteen years at that rate. With 50% higher expenses, that $2.5M nest egg doesn't seem quite so adequate.

- Investing so conservatively, that a portfolio does not grow at a sufficient pace to offset inflation. Many people cannot bear the daily ups and downs of the stock market. Instead they choose an ultra conservative portfolio of CDs, money market and other fixed income investments that will provide a lower, but steady return. Even though the nominal return may be steadily positive, the real return of such a portfolio is anything but steady and positive. At its best the ultra conservative portfolio will barely outpace inflation. At its worst, this combination of investments will leave the investor with less and less purchasing power over time. As Larry Swedroe points out: "The lesson we take from the historical evidence is that those seeking to avoid investment risk may incur the even greater risk of the loss of their purchasing power over the long term. The bottom line is that in terms of achieving financial goals, the return from riskless instruments may likely to prove insufficient." The only ways a person can effectively compensate for the lack of real growth in their portfolio is to lower their expectations for the future, or save more--generally a lot more. Unfortunately, not many people are willing to do either of these.

- Not understanding the significance of cost-of-living-adjustments (COLAs) on pensions, annuities, and Social Security. Imagine two friends retiring the same year from two different employers. Ed considers himself very lucky, and will get a $4,000 per month pension from a private sector employer. Like most private sector pension plans, Ed's pension does not include any inflation adjustments. His neighbor, Ralph will also be receiving a $4,000 per month pension from a public sector employer, and it will have annual COLA adjustments. In year one the two friends feel equally happy, have a similar lifestyle, and they enjoy the same purchasing power from their healthy pensions. However, after twenty years averaging just 3% inflation, Ralph will be receiving about $7,200 per month, but Ed will still be receiving $4,000. Those two pensions, which seemed so equal at the beginning, are anything but equal. A pension or annuity that does not have any provision for inflation adjustment is worth much less than one that does. If inflation is low, the difference will take a while to show up. However, just a few years of extremely high inflation, such as experienced in the 70's and early 80's, will wreak havoc on the fixed pension. The impact of inflation on a fixed pension should be anticipated from the start, but a lack of planning for the inevitable decline in purchasing power is a common mistake.

Social Security is an inflation adjusted pension or annuity that most Americans will benefit from in retirement. Discussions are underway about the right methodology for determining future Social Security COLAs, and these changes will likely result in somewhat lower future inflation adjustments. However, even with some tweaks to the calculation, people should continue to receive tremendous value in having a basic foundation of inflation adjusted retirement income through the system.

Of course, we don't know exactly what inflation rates will be in the future, but we hopefully know enough to plan. Investors need to realize that there is a certain level of inflation expectations implicitly or explicitly built into the prices of stocks, bonds, and other investments. It is important to always consider the difference between the nominal return to investments, and the real return. Higher nominal rates of return may sound better, but real rates of return will determine your future lifestyle. The big risk to our financial plans is if inflation rates deviate significantly (up or down) from the somewhat low inflation expectations built into current stock and bond prices. Protecting yourself from both expected and unexpected inflation is a key objective of portfolio construction.

In later posts we will look at the Consumer Price Index--some of the controversy around it, and why your personal inflation rate may look very different from the averages.

If holding too much employer stock is so risky, and so many authorities warn against it, why do so many people continue to invest their retirement savings in the company they work for? These are the employees of America's great corporations, the engine of the world's mightiest economy--they can't all be simpletons!

If you have occasion to read books or articles on the subject of behavioral finance you will probably notice how often the issue of company stock is used as an example for a variety of behavioral biases-or ways which investors act less than rationally or optimally. Here are a few examples of relevant investor biases:

- Home bias is the tendency to believe that familiar investments are the best. Many people are simply more comfortable investing in what they perceive they know best. And, what do we know better than our own company? In Your Money and Your Brain, Jason Zweig sites a 2001 study of 401K investors where only 16.4% of them believed their company stock was riskier than the stock market as a whole. This is certainly contrary to portfolio theory and conventional wisdom that a diversified portfolio of stocks is less risky than a single stock.

- Closely related to home bias is something called ambiguity aversion bias--basically that people dislike uncertainty more than they dislike risk. A person feels they have an understanding of the risk they are taking with their own company, but haven't a clue what is going on at all those other companies, or the market as a whole. Zweig relates a funny story about how while giving a talk and cautioning investors on the perils of investing in their own company stock, and citing the recent Enron example, a guy in the audience stood up and challenged him:

I can't believe what you just said! I completely agree that any company could be the next Enron. But that's why your advice makes no sense. Why should I move my money from the one company I know everything about to hundreds of stocks I don't know anything about? Diversifying doesn't protect me from the next Enron, it exposes me to every next Enron--and the stock market is full of them! I want my money where I know it's safe--in the company I work for and the company I understand better than any other one around. That's how I control risk.

- Also mentioned is optimism bias--basically, that people are just too optimistic and refuse to believe their own company could hit the skids like Enron. The Enron type scenario will certainly happen to other poor souls, but won't happen to me.

- Somewhat related to optimism bias, is confirmation bias, where people put too much weight on information or data that supports what they want to believe. They believe positive commentary about their company and its prospects--basically because they want to believe--and discount negative news. (They drink the company Kool-Aid.) People rationalize their concentrated holdings of company stock because of "big things coming down the road". A sad example are the employees who doubled down on Enron stock in late 1999 after their human resources director responded to the question, "Should we invest all of our 401K in Enron stock?" with a resounding: "Absolutely".

- Since many investors receive company stock as a matching or profit sharing contribution, they are susceptible to the endowment effect. The endowment effect is where you value a thing or asset that you own, more than when you don't own it. Basically, even though you would likely not have purchased the company stock if you had been given the equivalent cash in the first place, you are now reluctant to sell the stock at a fair market price. Not only is there an implicit company endorsement of the stock when your company gives it to you, but there is this aversion to selling and diversifying away from it. The endowment effect is powerful--according to Vanguard, 401K plans that make matching contributions in company stock have 3.3 times more assets held in company stock than those that don't (37% versus 11%).

There are, of course, other reasons why people end up having relatively high concentrations of their employer stock. Many people participate in employer stock purchase plans where they receive a significant discount on the purchase price. There may be restrictions on how soon an employee can sell the stock, and then there are tax considerations on the sale. Other employees may receive large blocks of stock options or restricted stock, which have a vesting period and are then subject to substantial taxation. By delaying the exercise of options, or the sale of stock, the employee is delaying taxation, which is generally considered a good thing. All this employer stock can add up to a substantial percentage of a person's net worth.

Inside or outside a 401K plan, there is at least one more good reason why many hold sizable percentages of their net worth in company stock. It often works out very well for many people. Most of us know, or know of, folks who have done very well due to working for a successful company and dutifully buying and holding the company stock. Water cooler talk about how Larry bought his lake house with the money he made on stock accumulated through a share purchase plan, or how Ruth retired early after cashing in on her options, make your company stock look like a pretty smart investment. And, it just may be.

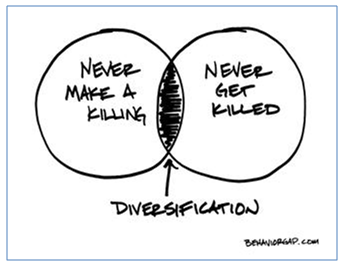

The problem with holding too much company stock isn't that you can't be successful. You obviously can be. You can be very, very successful. The problem is you can also lose big, possibly losing your job at the same time. When you hold a concentrated position in company stock (or any one stock) the range of outcomes is simply much broader (from very bad to very good) than when you are highly diversified portfolio of hundreds of stocks. Or, as Carl Richards recently described being diversified: "Never make a killing. Never get killed." When approaching the decision on how much company stock to hold, you need to decide whether you want the chance to get somewhat richer while accepting the risk of ending up significantly poorer. As for me, I would choose to diversify, hoping to have "enough" to meet my reasonable financial objectives, while minimizing the chance of ending up poor.

The perils of holding too much of your employer's stock is widely acknowledged in financial planning circles. In Part 1 the key reasons why you should seriously consider diversifying away from your company's stock are outlined. If you are not convinced, ask yourself why defined benefit pension plans (old style pensions where investment professionals manage money set aside in trusts to fund the retirement of employees) are restricted by law to hold no more than 10% of their assets in company stock? If it is not wise, or lawful, for pension professionals to invest too much in company stock, do you really think it is a good idea for you to do so?

The fear of litigation stemming from employees stung by major drops in company stock, along with new diversification guidelines set forth by the Pension Protection Act of 2006, has encouraged 401K plan sponsors to make it easier for plan participants to diversify away from employer stock. Although the concentration of employer stock in 401K plans has decreased over the last several years, it is still a notable risk for many investors preparing for retirement. At several large, well-respected companies employees still hold remarkably high percentages of their retirement plan assets in employer stock. For example:

- Proctor and Gamble employees reportedly hold over 90% of their 401K plan assets in P&G stock.

- General Electric employees still hold 40%, even though GE's stock price is essentially at 1997 levels. (Granted, there have been some major ups and downs since then!)

- ExxonMobile employees, who hold about 65% of their 401K assets in company stock, undoubtedly breathed a collective sigh of relief when it was a BP well, not one of their own, that blew out in the Gulf of Mexico. ExxonMobile is up about 25% over the last year, while BP was down over 50% at one time in 2010. Almost 30% of BP's 401K assets were in its own stock.

If you are still holding a significant (e.g. >10%) share of your retirement savings in your company's stock, you are certainly not alone. Separate studies from the Employee Benefit Research Institute (ERBI) and the Vanguard Center for Retirement Research show the following:

- Large companies are more likely to offer company stock as an investment option than small companies. Even though the vast majority of 401K plans do not have employer stock as an investment option, a sizeable proportion of overall plan participants (46% in the ERBI sample and 36% in the Vanguard study) do have company stock as a choice. In plans where it is an investment option, the ERBI study found about 20% of total plan assets invested in company stock.

- Of those participants who have company stock as an option, close to 50% (ERBI=48%, Vanguard=45%) are wise and choose to hold none of it. (We can only assume they are avid readers of financial planning blogs such as this one.)

- Although the majority of participants with company stock as an option hold only reasonable amounts (<20% of their 401K balances), there are still a sizeable minority with dangerously high holdings. About 30% of participants hold more than 20% of their portfolio in company stock, and there are 5 to 10% of participants holding almost all (> 80%) of their retirement funds in employer stock.

A Potential Tax Benefit to Company Stock

Before you rush off to reallocate your 401K investments, be aware of one potentially advantageous tax strategy available to you if you hold highly appreciated company stock in your employer sponsored plan at retirement. It is called "net unrealized appreciation", or NUA. Basically, the NUA strategy allows you to separate out your company stock from the rest of your 401K assets and immediately pay ordinary income tax on the cost basis of the stock (i.e. what you originally paid for it). Then, when you decide to sell the stock, you will pay only the long term capital gains tax rate on the appreciation. The end result of choosing NUA taxation may be more favorable than keeping the assets in the plan or rollover IRA, where you will eventually pay ordinary income tax on the entire amount when withdrawn. This strategy is complicated, and the IRS is reportedly unsympathetic to those who don't execute it according to the rules. If you think you are a candidate for NUA, definitely do your homework and plan on consulting with a qualified financial advisor or your tax professional prior to rolling over your retirement plan. (For a detailed review of NUA see this 2007 white paper from the Fidelity Research Institute.)

In Part 3, we'll look at some of the reasons put forward as to why people choose to hold so much company stock in their 401K.

Enron is the poster child of the employer stock double whammy--lose your job, lose your life savings. At the end of 2000, Enron employees held on average 62% of their 401K assets in Enron stock. The stock price peaked at $90 per share in August 2000, and employees were feeling smart as they watched their account balances soar. By the end of 2001, Enron had filed for bankruptcy, many employees had lost a significant portion of their retirement savings, and over 95% of them had lost their jobs.

This couldn't happen to you...or, could it?

As it turns out, Enron isn't the only example of a company imploding and giving employees the double whammy--it is just the most memorable. A number of other companies, bankrupt or near bankruptcy, have experienced significant job losses while employee 401K balances tanked due to high allocations in falling employer stock. These include Countrywide Finance, Color Tile, Lucent, and (my favorite) Bear Stearns. You would expect those highly paid financial professionals at Bear Stearns would have been savvy enough to diversify away from their own company stock, but apparently many were not. Of course, if they were such smart money managers, maybe they would have seen what a precarious position their own company was in.

Maybe your situation is different. You feel your job is safe and your company stock has been an excellent investment. What is so wrong with holding a significant portion of your net worth in your employer's stock? Please consider these reasons why it may not be such a great idea.

- First, a concentrated position in any one (not just your employer's) stock results in you taking more risk than you are being compensated for by the expected return on your investment. In finance-speak, you are taking on "unsystematic risk" that can, and should, be diversified away--without lowering your expected return. You are missing out on one of the only free lunches available to the common investor! Although the risk you are taking with a significant allocation to one stock may be difficult to grasp, here are a couple of data points to consider:

- On average, the price volatility (as measured by standard deviation--the most common metric of stock risk) is at least 2.5 times higher for a single stock than for a highly diversified portfolio of stocks.

- Although a single stock may significantly out-perform a diversified portfolio, it is much more likely (on average) for a single stock to under-perform the market by a wide margin. For the twenty years from 1984 to 2003, only 6% of the stocks in the S&P 500 significantly out-performed the average by more than 5% per year. On the downside, however, 27% of the stocks underperformed by more than 5% per year. For every big winner, there were more than five big losers.

- Second, even if you decide a concentrated position in a single stock is a still a good idea, why would you choose your employer's stock? Imagine someone is holding a gun to your head and forcing you to choose one single stock to invest over 50% of your life savings in. However, they are very nice about it and let you choose this single stock from the over 5,000 exchange traded stocks in the U.S. They even give you ample time to research and choose the one single stock that gives you the best balance of risk and expected return--after all, this is your retirement nest egg we are talking about. What are the chances that the one stock you choose to gamble your life savings on, out of this cornucopia of choices, just happens to be the company who employs you? Talk about coincidences! Do you really think the stock of the company you work for is the best you can do? (Come on--anyone who is even marginally paying attention at work is pretty aware of how screwed up things are at their own company. There must be times you think you are working at the same company as Dilbert.)

- Finally, your human capital, or earning power, is arguably your biggest asset and currently "invested" with your employer. Do you really want your financial capital and your human capital all invested in the same place? Many people just don't realize the risky position they have put themselves in.

- Most would agree that losing a job is both emotionally and financially difficult for a person and their family. It is one of those big risks in life that the average person needs to consider and prepare adequately for.

- Most would also agree that losing a big portion of your investable assets can be terribly upsetting. Not only could it set back your retirement plans by many years, but it could significantly impact your lifestyle today and in the future.

- Now, for an unsettling vision, imagine these events happening in the same week. Imagine your spouse, who trusted you with the investment decisions, looking at you in shock and dismay as the circumstances unfold. Unfortunately, the risk of you losing your job and the risk of your company stock falling off a cliff are positively correlated--but, you don't have to expose your family to this double risk.

The risk of holding too much company stock has always been obvious to some. And, due to the well publicized events at Enron and elsewhere, many others have taken steps to diversify their portfolios. However, the risk of over concentration in employer stock still exists. We'll look at it further in Part 2.

Although you may be extremely confident that you don't suffer from the financially destructive behavioral bias of overconfidence, you may have a friend who could benefit from a little advice on dealing with this tendency. Here are a few suggestions to consider.

- Recognize the danger. Acknowledge that overconfidence can be hazardous to your financial well-being and that you too can be susceptible to its effects. Obviously, we need enough confidence to move forward and make decisions in our financial life. However, just like a lot of things in life (e.g. food, alcohol, reading financial blogs), moderation is key. Recognize your limitations, and don't overestimate your skills, knowledge, and predictive capabilities. A little humility is not only an attractive quality in a person--it is a necessary condition for successful financial planning.

It's not what a man don't know that makes him a fool, but what he does know that ain't so.--Josh Billings, nineteenth century American humorist

- Men, listen to your wives. If behavioral researchers are correct, your wife is less likely to be an overconfident investor than you are. And, it is a safe bet that she is not as confident in your investing ability as you are. Use this to your advantage and consult your spouse on investment strategy and decisions. (This goes both ways, obviously. Women, consult your husbands.) It could just be that two heads are better than one, and two ways of looking at things may result in more wisdom and understanding. Sure this takes longer, but the joint decision-making and buy-in is a positive thing. Besides, taking longer isn't necessarily a bad thing. My guess is that the bad, impulsive decisions you avoid will more than offset the few time-sensitive opportunities you miss.

An excellent wife, who can find? For her worth is far above jewels. The heart of her husband trusts in her, and he will have no lack of gain. --Proverbs 31: 10-11

- Benchmark, document and review. Check your investment performance against relevant benchmarks and determine if you are really as capable as you think. Also, write down your reasoning for buying or selling a particular investment, and check it later. (Do this right away, since your recollection of your reasoning will be tainted by the passage of time.) Or, if you dare, write down your predictions for the economy and the financial markets. Were you right about that company's prospects, that interest rates were set to rise, or that the market was set for a correction? How good did you do--not just your investments, but your reasoning? We all tend to have some "hindsight bias", so this documentation helps us to see if our investment performance was really that good, or if our predictive abilities were as acute as we remember. You may outperform the benchmarks sometimes, and your predictions and reasoning may have been right on target. However, you will undoubtedly underperform for periods, and your forecasts may be laughable at times. This documentation will encourage a bit of humility, and serve as a sobering reminder of how difficult it is to be consistently right.

Prediction is very difficult, especially if it's about the future. --Nils Bohr, Nobel laureate in Physics

- Keep track of your mistakes. In Your Money and Your Brain, Jason Zweig recounts how Christopher Davis of Davis Funds has the "mistake wall" outside his office. This is where his company's worst investments are memorialized. For Davis, mistakes are bad decisions that could have been prevented with better information or better analysis. The key thing here is the practice of recognizing, remembering and learning from your mistakes, rather than suppressing and denying them. Your own personal mistake wall or folder will not only remind you of your limitations, but of those lessons you have learned and paid for.

All men make mistakes, but only wise men learn from their mistakes.--Winston Churchill

Experience is that marvelous thing that enables you to recognize a mistake when you make it again.--Franklin P. Jones

Michael Pompian in Behavioral Finance and Wealth Management points out that an important implication of overconfidence is that it may leave many investors ill prepared to meet their future objectives, whether it is funding college for their children or replacing their income in retirement. He claims:

...most parents of children who are high school aged or younger claim to adhere to some kind of long-term financial plan and thereby express confidence regarding their long-term financial well-being. However, a vast majority of households do not actually save adequately for educational expenses, and an even smaller percentage actually possess any "real" financial plan that addresses such basics as investments, budgeting, insurance, savings, and wills. This is an ominous sign, and these families are likely to feel unhappy and discouraged when they do not meet their financial goals.

Don't let overconfidence contribute to you being financially unprepared for your future and the disappointment it will bring. Invest the time and effort in creating a realistic financial plan that will give you a good shot at meeting your objectives. Contact Table Rock Financial Planning, or another hourly, fee-only advisor from the Garrett Planning Network to assist you in this effort.

Many researchers, and all the women that I know, believe that men are more likely to be afflicted with the wealth destroying trait of overconfidence. Terrance Odean and Brad Barber gave support to this argument in their 2001 paper entitled, "Boys Will Be Boys: Gender, Overconfidence, and Common Stock Investment". Their real point was not that men are total idiots, although I'm sure there is ample research somewhere to support this thesis. Their claim was that men traded more often, presumably due to overconfidence--a trait that psychologists associate with men in manly-man* areas such as finance. In fact, their study showed men trading 67% more actively than women.

Odean and Barber's previous research, including "Trading is Hazardous to your Wealth: The Common Stock Investment Performance of Individual Investors" had demonstrated how excessive trading led to significantly lower returns for individual investors who traded stocks more frequently. Men and women both traded too much, and underperformed a buy-and-hold strategy. However, men underperformed women by an additional 1% per year, presumably due to the additional trading.

Even John Ameriks, head of Vanguard Investment Counseling and Research, has bought into the "men are overconfident" line of thinking. He said, "There's been a lot of academic research suggesting that men think they know what they're doing, even when they really don't know what they're doing." However, I'm not so sure his recent research really supports this conclusion, but it earned him a mention in a recent NY Times article. The Vanguard research showed that men were 10% more likely to abandon equities in the 2008-2009 market downturn, which although statistically significant, was not nearly as important as the differences in other criteria (e.g. age, and type of investment vehicles). As Brad Barber commented regarding generalizations about investor behavior, "The differences among women and the differences among men are much greater than the differences between men and women."

Even if men demonstrated a higher propensity to abandon equities during a downturn, this is hardly a sign of overconfidence. Wouldn't an overconfident man (I mean a real manly-man) stick with his stock investments when the going gets tough? Wouldn't it be the man who lacks confidence (a girly-man) who sells out at the market bottom. Doesn't selling as the market bottoms out just scream, "Boy, did I screw up, honey!" Wouldn't the real manly-man feign confidence and reassure his wife, "This is just the sissies selling out. These stocks will come back. I know they will."

Fortunately, more research is being done on this matter. According to Brian Knutson of Stanford University, new brain imaging technology is making it possible to determine exactly "what is happening in the brain before people make financial decisions." Who needs brain imaging technology? Any woman can tell you what the real manly-man is thinking before deciding to buy the next hot stock, or sell out as that investment plummets.

He's thinking about sex...and he's overconfident.

See Part 3, Dealing With Overconfidence.

===================================================

*According to a Recognized Internet Authority, men may be overconfident--but, we do it for women. Topping the list of "10 Ways To Be A More Manly Man" is:

1. Confidence--Honestly, confidence is number one for a reason. Girls generally don't think men are manly if they don't have any confidence and even guys that are total dweebs, in many cases, can still attract gals by displaying this characteristic. Ways that guys can better gain and have confidence is by being happy about who you are and just being yourself (as cheesy as it sounds).

Although a healthy self-image and a bit of self-delusion are generally a good thing--and arguably necessary in starting a new business venture or while asking a cheerleader for a date--overdoing it isn't beneficial in investing. As Jason Zwieg observes in Your Money and Your Brain:

A pinch of confidence encourages you to take sensible risks and keeps you from storing all your money in the concrete bunker of cash. But if you think you're Warren Buffet or Peter Lynch, your inner con man is not telling little fibs; he's a big fat liar. You will never make the most of your investment potential if you think you have far more potential than you actually do. The only way to achieve everything you are capable of is to accept what you are not capable of.

Overconfidence in investing is a recipe for underperformance. Just like the 93% of us who believe we are above average drivers, many of us think we are more capable investors than we really are. Just as in Lake Wobegon, where "all the women are strong, all the men are good looking, and all the children are above average"--most of us seem to think we can beat the market.

When asked why people think they can beat the financial markets, Nobel Prize winner and behavioral economics pioneer Daniel Kahneman answers: "I do believe the answer in most cases is that people think they are better than anyone else--optimistic bias." This optimistic bias leads people to take risks they wouldn't take if they knew the real odds of success.

Kahneman often refers to "delusional optimism", where "people do things they have no business doing because they believe they will be successful." People are overconfident, often exaggerating our knowledge and over-estimating the amount of control we have over outcomes. We under-estimate what we don't know and downplay the role of chance. He explains, "We distinguish between games of skill and chance, but we see life as a game of skill. People tend to deny the role of chance: we see that in many studies of executives." This is why entrepreneurs believe they will succeed, even if they are aware of the enormous odds of failure--at least the odds of failure for all those other, less skillful entrepreneurs.

Overconfidence may well be a key driver in moving capitalism forward--or downward, as we have seen over the past few years. But for individual investors overconfidence can be a wealth destroyer, deceiving them in many ways. It often leads to taking on too much risk, because we over-estimate our odds of success. We may invest too much in that which we are most confident or familiar (e.g. company stock--think Enron). We may over-estimate our ability to evaluate a stock or other investment, and discount the abilities of the countless MBAs at Goldman Sachs and other Wall Street firms who are invariably on the other end of every trade we make.

One of the funny things about the stock market is that every time one man buys, another sells, and both think they are astute. --William Feather

However, as Terrance Odean points out in this article, the two biggest investing issues stemming from overconfidence are excessive trading and lack of diversification. Research by Odean and Brad Barber, appropriately titled "Trading is Hazardous to Your Wealth", showed how a large sample of active traders under-performed buy and hold investors by an incredible 6% per year. (More on Odean and Barber's research in Part 2.)

Diversification is a well understood tenet of wise investment. With an under-diversified portfolio, you are simply taking more risk than necessary for the expected return. Portfolio theory explains investors are compensated only for systematic risk, not the unsystematic risk that can be diversified away. Overconfident investors ignore this, or maybe have never have understood it, and hold too much of their pet investments. They believe they know more than "the market". Sure, they can strike it big, but they can also lose close to everything.

Diversification for investors, like celibacy for teenagers, is a concept both easy to understand and hard to practice. --James Gipson, former manager of the Clipper Fund

Of course, not everyone suffers from overconfidence or delusional optimism. I would argue that Kahneman (U.C. Berkeley, PhD-1961, and professor 1986-1993), Odean (UC Berkeley, BA-1990, MS--1992, PhD-1997, and Professor of Finance, 2001-present), and myself (UC Berkeley, MBA, 1981), have all been inoculated from the scourge of overconfidence by our association with the Golden Bears football team. This is a team whose only noteworthy achievement since going to the Rose Bowl in 1959 was THE PLAY. However, we likely suffer from a related bias--irrational optimism (not to be confused with irrational exuberance). We know that miracles have happened in the past, and just may happen again. Cal may play Boise State for the national championship, the U.S. may win the World Cup, and my old HP stock options may someday be above water.

See Part 2, Women are Rational, Men are Overconfident.

Next page: Disclosures

{kind=link}