Financial Planning Blog

Measuring inflation is a dauntingly complex task, as we saw in Part 2. But with Social Security benefits, pension payments, tax brackets, investment and insurance products, not to mention a host of labor and other contracts all linked to an "official" inflation rate, it is a measurement that impacts everyone's pocketbook. One can't help seeing a parallel with a similar statistical mystery--the Bowl Championship Series. Football fans in Idaho are well acquainted with that politically deceitful, statistically convoluted black box that can be counted on each year to send Boise State to the Little Sisters of the Poor Bowl while schools with proper pedigrees divide the financial spoils of the BCS. (See this video on What If Everything Worked Like the BCS--The Spelling Bee.)

We know the BCS is complicated. We know the BCS is crooked. We've almost learned to live with that. But, could it possibly be that measuring inflation is even more complicated than the BCS...and just as crooked?

"There are three kinds of lies: lies, damned lies, and statistics." - Mark Twain (attributed to Benjamin Disraeli)

Unless you are into anti-government conspiracy theories--after all this is Idaho, and we do love to hate the Feds--you may never have given much thought to the possibility that the official inflation numbers published by the Bureau of Labor Statistics (BLS) have been manipulated to your detriment. Over the last few decades the BLS has made important changes to how it calculates the CPI that significantly lower the reported inflation numbers. This is no secret, and the methodology and impact of these changes is well documented. There is considerable controversy, however, as to whether these changes were appropriate, or part of a complex plot to lower the official CPI estimates to order to minimize inflation's apparent impact. And, more importantly, minimize the on-going increases of government expenditures linked to the CPI.

First, a quick summary of the controversial changes in CPI measurement:

- In 1983 the way the changes to cost of owner-occupied housing is measured was significantly modified. A new measurement called owner's equivalent of rent (OER) was substituted for the change in actual housing prices. OER measures the amount a homeowner would have to pay to rent their home, or alternatively would earn by renting their house out in a competitive market. The reasoning behind using OER instead of house prices is that owner-occupied housing consists of both a consumption element and an investment element, and the CPI is designed to exclude investments (e.g. stocks, bonds, real estate.) This is certainly reasonable when you consider that contrary to other price increases, homeowners are usually very happy when the values of their homes rise. There is no arguing that using OER instead of house price changes has resulted in a much more stable index. For example, since 2000 housing prices changes as measured by the Case-Shiller Index have swung wildly between +20% and -20% per year, while OER has moved in a narrow range between 2% and 5%.

- In 1999 the BLS began using a geometric mean formula in the calculation of the CPI. This methodology seeks to reflect consumer substitution behavior, where people make trade-offs on the basis of both price and personal preferences in an effort to maximize their standard of living. Critics claim that if the price of filet mignon goes up, and consumers switch to hamburger, the BLS simply substitutes hamburger for steak and calls it even. The BLS adamantly denies this type of substitution is made, and makes a very reasonable defense. (For an understandable, but lengthy explanation of these changes and other see this 2008 BLS article--Addressing Misconceptions about the Consumer Price Index.)

- Starting in 1998 and phased in over time are hedonic (derived from the Greek word for pleasure) statistical models that adjust for quality changes. Using multiple regression analysis the value of new features or quality changes is estimated by comparing the prices of items with and without that feature. Basically, the BLS is trying to estimate what portion of a price increase (or decrease) is due to quality changes, and whether the consumer is left better or worse off. (Again, see the BLS article for a good explanation.)

On one side of the inflation controversy are economists that contend that the CPI for years was systematically overstating price levels to the tune of 0.8% to 1.6% per year. These were the findings of the Boskin Commission, appointed by the Senate Finance Committee in 1995 to study the effectiveness of the CPI estimates, finally resulting in the late 90's changes mentioned above.

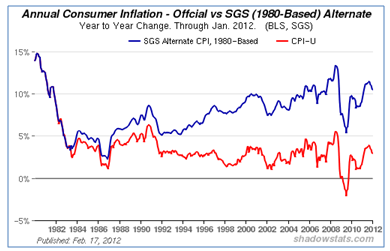

In the other camp are those that believe the pre-1982 methods of measuring inflation would give a truer picture of the debasing of the dollar and the impact of price changes on people's well-being. A well known, vocal proponent of this point of view is Walter J. "John" Williams and his work can be found on his Shadow Government Statistics website. Here is his 2006 take on the changes to CPI measurement:

The CPI was designed to help businesses, individuals and the government adjust their financial planning and considerations for the impact of inflation. The CPI worked reasonably well for those purposes into the early-1980s. In recent decades, however, the reporting system increasingly succumbed to pressures from miscreant politicians, who were and are intent upon stealing income from social security recipients, without ever taking the issue of reduced entitlement payments before the public or Congress for approval.

In particular, changes made in CPI methodology during the Clinton Administration understated inflation significantly, and, through a cumulative effect with earlier changes that began in the late-Carter and early Reagan Administrations have reduced current social security payments by roughly half from where they would have been otherwise. That means Social Security checks today would be about double had the various changes not been made. In like manner, anyone involved in commerce, who relies on receiving payments adjusted for the CPI, has been similarly damaged. On the other side, if you are making payments based on the CPI (i.e., the federal government), you are making out like a bandit.

According to Shadow Stats, the current annualized inflation rate, measured using older pre-1982 methodology is about 10.5%, compared to the official rate of a little over 2.9%--over 7% higher!

Ignoring the 1983 housing change, the cumulative impact of the other methodological changes is less dramatic, but still significantly large enough to be make a major dent in the COLA adjustments to your government check.

Are Williams and other critics right, and the federal government is manipulating statistics to hold the official inflation down? I'm not qualified to pass final judgment on the BLS statisics, but I have to say their methodology seems OK to me. For one thing, if the Shadow Stats' numbers were used and Social Security and government pensions were all about double today's level--does that even pass the smell test? It's not like wages and salaries have been rising at a screaming pace. Does it seem right that Social Security benefits and pensions should be rising at over 10% per year? I don't think so.

Just because inflation used to be calculated one way, doesn't mean that is the way it should be done in perpetuity. Just because cost-of-living increases were calculated in the 70's using the old way, doesn't mean it's a good idea for the new millennium. And, just because college football has always had a corrupt bowl system where elite colleges meet to crown a champion and divide the TV money, doesn't mean that is the way it always has to be.

Like the CPI, we should give economists a chance to redesign the college football post season and bring it into the 21st century. One thing for sure, it would certainly look different than the current BCS. Unfortunately for BSU, however, the championship will likely still require kicking a field goal.

In Part 1, the necessity of thinking clearly about inflation was stressed, along with planning for future inflation rates. (For more on this, also see this recent Morningstar article.) However, as it turns out, just figuring out what the current inflation rate is turns out to be much more complicated than most people realize.

Determining price levels and the rate of inflation is not as simple as measuring other things. For example, when you weigh yourself in the morning you just step on the scale and get a nice digital readout. There are, of course, some similarities between prices and our weight--a lot of short term ups and downs, but generally a small percentage movement up and to the right every year. But, think about it. If you are trying to measure price movements, the first question is the price of what? Each of us spends our money on so many different goods and services over the span of a year, and each of us spends our money different than the next guy. If gasoline goes up 5%, and bread goes down 5%, and milk stays even--what does that say about inflation? What if light beer goes down in price, but microbrews go up 5%? What if cable TV goes up so darn much you drop it altogether, saving $100/month?

In order to get a handle on price changes the U.S. Bureau of Labor Statistics goes to great effort to construct two major categories of price indexes. The first set, which we will ignore for the purposes of this discussion, are the Producer Price Indexes which measure price changes from the perspective of producers along various points of the supply chain. The second set of indexes is the Consumer Price Index, which measures changes from the perspective of the end-use consumer. This is the most familiar, and has the most impact on most of our everyday lives. A quick scan of this document from the BLS tells you the first thing you need to know about inflation--it is an incredibly complex measurement that must take an army of economists and statisticians to pull together.

- Price data is collected every month from over 4,000 homes and 26,000 retail and service establishments of all kinds, in 87 different urban areas across the United States.

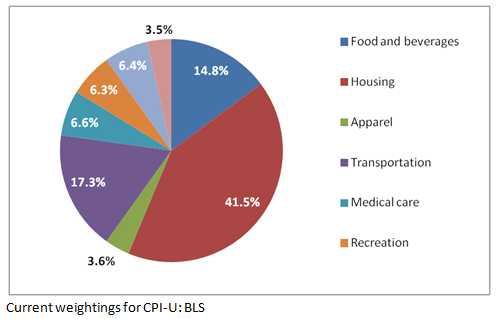

- Prices for goods and services are collected in 8 different major expenditure groups, and these are further divided into about 200 subgroups. Each subgroup has a representative market basket containing hundreds of specific items from specific retail establishments. In all, data on about 80,000 different items is collected in scores of different cities across the country. We're talking soup-to-nuts, mutton to motor oil, frankfurters to floor coverings, from Brockton to Bremerton and Saint Pete to San Fran.

- These representative market baskets were developed from major surveys of thousands of consumers--the last ones back in 2007 and 2008. Detailed diaries and interviews were used to determine the content and relative weighting of the over 200 subgroups. The relative weightings allow the BLS to get compute the index, which is a weighted average of all the items measured. This weighted average may be a good representation of the average consumer, but your individual market basket is undoubtedly very different. The current relative weightings of the eight major expenditure groups are shown below.

But wait, that's not all. You may not have realized there isn't just one CPI number--that would be too simple. There are actually a number of Consumer Price Indexes calculated. These indexes are calculated regionally, then averaged for the country. Also, the indexes are published in both seasonally adjusted and unadjusted form. If you are making any decisions from this data, you want to be careful to understand what you are looking at. Below are the key indexes you likely will see quoted in different contexts.

- CPI-W: The CPI for Urban Wage Earners and Clerical Workers, a collection of households that represent only about 32% of the population. This is an older index with a limited subset of households (wage earners and clerical workers), but is important because it is the one used by the government to adjust Social Security payments on an annual basis.

- CPI-U: The CPI for All Urban Consumers, which covers about 87% of the total US population. This is a superset of the CPI-W, adding many additional categories of workers (e.g. the self employed and professional, managerial, and technical workers), along with the unemployed and retirees. (It is interesting to note that SS payments are adjusted by an index that excludes retirees, the CPI-W. I'm sure this makes sense to someone in the government.)

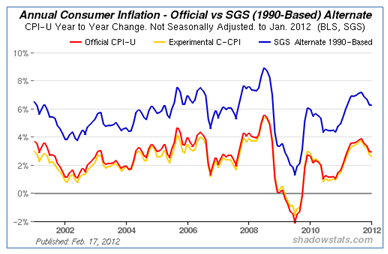

- C-CPI-U: Chained CPI for All Urban Consumers which covers the same set of households as the CPI-U, but uses a different methodology that attempts to reflect substitutions and adjustments consumers make as prices change. There are serious discussions underway to use the C-CPI-U to base adjustments to Social Security benefits, government and military pensions, and tax brackets. The chained CPU approach results in a lower inflation adjustment, and thus would lower government payments over time, along with potentially securing more revenue through slow, stealthy tax increases. (Needless to say, not everyone is a fan of this idea. More on that later.)

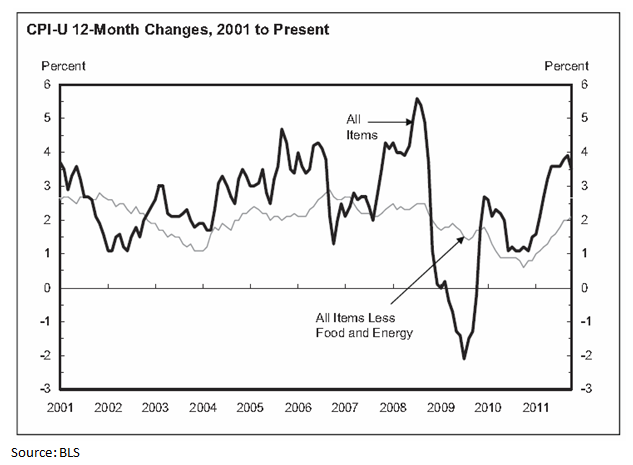

- Core CPI: This is an inflation measure that removes the effect of the volatile food and energy components of the CPI. Since food and energy account for close to 25% of the CPI, and often have major short term swings, removing these items results in a major smoothing of the curve, and helps economists observe inflation over the remainder of the economy. The Federal Reserve pays close attention to this number in its role of keeping inflation within desired bounds. The core CPI is often contrasted with the "headline" CPI, or CPI-U. When you hear an inflation number that is totally out-of-sync with what you are experiencing, listen carefully. It is probably the Core CPI that is being quoted.

- CPI-E: This is a CPI measure the attempts to reflect the different "market basket" or spending habits of the elderly. It is an experimental BLS inflation statistic, and you probably haven't heard much about it. However, senior advocates would like the concept to catch on. The argument is that certain categories that older Americans spend more money on, especially healthcare, are underrepresented by the CPI-W. If Social Security was indexed to the CPI-E, cost-of-living increases would, in theory, better represent what seniors experience. And, more importantly, benefits would be presumably higher.

A couple of key points about inflation should be obvious by now. First, it is impossible to get an exact read on what inflation really is. The BLS goes to great effort, and probably does a superb job, but like most statistics about the economy it is an elaborate estimate that takes on the cloak of accuracy. Second, no CPI is going to measure your exact experience with price increases. You experience somewhat different inflation than your next door neighbor (the one drinking light beer while you sip your microbrew), not to mention the retiree in Florida, the oil worker in North Dakota, or the single mother in New Jersey.

What may not be obvious from all of this is the government conspiracy that is currently gaming the inflation numbers. (Yes, this is playing to the local crowd, but the best way to get Idaho readers to continue to the next post is to mention a government conspiracy or complain about the BCS. You get both in Part 3.)

It may come as a shock to you, but apparently some financial advisors have made mistakes with their own money. Some will even admit to their financial blunders--to family, friends, colleagues, or even clients. However, a financial advisor with an inclination to own up to his errors in personal financial management should probably think twice before coming clean in a New York Times article. Just ask Carl Richards.

Carl Richards is a Certified Financial Planner and investment manager in Park City, Utah (formerly located in Las Vegas, Nevada). He has developed quite a following for his "personal finance on a napkin" sketches and his personal finance blog posts at New York Times. (I truly look forward to seeing the latest sketch each week. But, really...who has time to read financial planning blogs?)

Experience is a hard teacher because she gives the test first, the lesson afterwards. -- Vern Law*

Richards' story is similar to millions of Americans'. He bought too much house in Las Vegas during the boom years. They borrowed too much off the equity to fund his business start-up, and live a bit better than they could really afford. After considerable soul searching, they stopped paying on the underwater home they could no longer afford, and eventually arranged for a short sale. You can hear Carl tell his story on a recent NPR Planet Money podcast.

Judging by the reader comments on the original article, Richard's struck a raw nerve for many people. Many cannot understand how a financial planner could make such mistakes, and still be an advisor. For example:

- "This article is incredible. The author isn't competent to manage his own financial affairs, and his job is advising other s how to manage theirs?"

- "The Times reaches a new low in the quality of its financial writers, and that's saying something. It's like it's a Times job requirement for them to manage their personal finances like a 7th grader."

- "The notion that Richards was, and still is, a financial advisor is an indictment of the entire industry. He is clearly incompetent. He made foolish choices based on avarice and now seeks to justify them."

- "My mechanic has more common sense about Finances. (No offense to my mechanic!) Wanna bet his next book and article is 'How I lost my Financial Business when I wrote about how stupid I was with my own Personal Finances in the NY Times'".

That is just a sampling of the negative comments fit to print. To be sure, there were also a number of readers who expressed positive sentiments. Many readers simply took the opportunity to tell a bit of their story of how the real estate downturn had affected them. And, a surprising number of humble folks took the time to explain how they were much better managers of their finances, much too wise, and much too moral to get caught in such a reckless fiasco.

Financial professionals have been debating the wisdom of Richard's mea culpa. Some believe he has harmed the profession and undermined the credibility of financial planners with the public. (Frankly, is that even possible?) Others see it as a breath of fresh air, and the start of number of useful conversations of how we all do stupid things with money, and how to avoid repeating them. I'm in the latter camp. The whole controversy has reminded me of the many mistakes I have made over the years, and how they have shaped the advice I give today. Just a few examples:

- I was in too big of a hurry to buy a house. I basically borrowed 100% at interest rates well above 10%. (It was the early ‘80s.) We should have been more patient, saved up a decent down payment, and waited for interest rates to drop to affordable levels.

- I didn't have the first house sold before starting to build the second house. It didn't sell, and we became accidental landlords. After a few years, we were able to finally sell, almost breaking even. Coming from California, I didn't realize you could lose money on real estate until then. Thankfully, my lesson was much less expensive than Carl's.

- While juggling two house payments, we had another child and I took a cut in pay due to the recession. We found out those house payments don't necessarily become easier over time. I discovered the wisdom of sufficient margin between your house payment and your income.

- Even though we had two children depending on us, we never had a will in place until much too late. We had plenty of excuses, but in retrospect this was really irresponsible.

- Too little life insurance. Too little emergency savings. Too much company stock. Too much stock in general.

- And, yes, even though I advise my younger clients not to do it--I borrowed money to buy cars. (It would have been easier to save up for them if I hadn't been paying on two houses. One mistake begets another.)

"Experience is a brutal teacher, but you learn. My God, do you learn." - C.S. Lewis

It just could be that our ability to learn from our own mistakes, and the mistakes of others, is the best thing financial planners have going for them. I thank Carl for encouraging me to reflect upon my past experiences, and reminding me to not be so darn smug and self-righteous about the "right way" to handle personal finances. Hopefully, financial advice delivered with a little more humility and a lot more understanding will be more acceptable, and ultimately more effective at improving the lives of clients.

------------------------------------------------

*Yes, the Vern Law from Meridian, Idaho. The Cy Young Award winning pitcher with the Pittsburg Pirates is also credited with saying, "A winner never quits and a quitter never wins." Who knew? I thought Coach Manship at Ladera Vista Junior High made that up.

Next page: Disclosures

{kind=link}